Delving into the realm of Business General Liability Insurance in 2025 opens up a world of crucial insights and foresight. This detailed exploration promises to shed light on the evolving landscape of insurance, providing a comprehensive understanding that is both enlightening and practical.

In the subsequent paragraphs, we will delve deeper into the various aspects Artikeld, offering a well-rounded view of what the future holds for business liability insurance.

Overview of Business General Liability Insurance

Business general liability insurance is a crucial financial safeguard for companies of all sizes, offering protection against various risks and liabilities that could arise during the course of business operations. This type of insurance helps cover legal costs, medical expenses, and damages associated with third-party claims of bodily injury, property damage, and advertising injury.

Purpose of Business General Liability Insurance

General liability insurance is designed to protect businesses from financial losses resulting from lawsuits filed by third parties. These lawsuits could arise from incidents such as slip-and-fall accidents on business premises, damage caused by products or services, or allegations of false advertising.

- Bodily Injury Coverage:This component of general liability insurance helps cover medical expenses and legal costs if someone is injured on your business premises or as a result of your business operations.

- Property Damage Coverage:General liability insurance also provides coverage for damage to third-party property caused by your business activities. This could include damage to a customer's property or rented premises.

- Advertising Injury Coverage:In the digital age, businesses may face claims of advertising injury, such as defamation, copyright infringement, or misleading marketing practices. General liability insurance can help cover the costs associated with defending against such claims.

Importance of Having Business General Liability Insurance

Regardless of the size or nature of the business, having general liability insurance is essential for protecting the company's assets and reputation. Without this coverage, a single lawsuit could result in significant financial losses that could potentially bankrupt a business.

General liability insurance provides peace of mind to business owners, knowing that they are protected in the event of unforeseen accidents or legal claims.

Trends and Changes in Business General Liability Insurance by 2025

In the evolving landscape of business insurance, several trends and changes are expected to impact general liability insurance by 2025. These changes are influenced by advancements in technology, evolving business practices, and potential regulatory shifts.

Emerging Trends in Business Insurance

As businesses become more digital and interconnected, the risks they face are also evolving. Emerging trends in business insurance include a greater focus on cybersecurity liability coverage to protect against data breaches and cyberattacks. Additionally, there is a growing demand for insurance products that cover intangible assets such as intellectual property and reputation risk.

Advancements in Technology

Technological advancements are reshaping the future of business liability insurance. The use of artificial intelligence and big data analytics is enabling insurers to better assess risks and customize coverage for businesses. Internet of Things (IoT) devices are also playing a role in risk prevention, as they can provide real-time data to predict and prevent potential accidents or losses.

Regulatory Changes

Potential regulatory changes could influence the coverage or cost of general liability insurance policies. For example, new data privacy regulations may require businesses to have specific insurance coverage to protect consumer data. Changes in tort laws or legal precedents could also impact the liability landscape, affecting the types of claims covered by insurance policies.

Impact of Emerging Risks on Business General Liability Insurance

Climate change, cybersecurity threats, and pandemics are all emerging risks that have the potential to significantly impact the landscape of business general liability insurance in 2025.

Environmental Risks: Climate Change

Climate change poses a major threat to businesses, as natural disasters and extreme weather events become more frequent and severe. This can lead to property damage, bodily injury, and other liabilities that may require coverage under general liability insurance. Insurers may need to reassess their risk models and pricing strategies to account for the increased likelihood of climate-related claims.

Cybersecurity Threats

With the rise of cyberattacks and data breaches, businesses are facing new risks that can result in financial losses, reputational damage, and legal liabilities. General liability insurance policies may need to evolve to include coverage for cyber-related incidents, such as data breaches and ransomware attacks.

Insurers may also offer specialized cyber liability insurance to address these specific risks.

Pandemics and Health Crises

The COVID-19 pandemic has highlighted the need for businesses to be prepared for health emergencies that can disrupt operations and lead to liability claims. Insurers may introduce new endorsements or exclusions related to pandemics in general liability policies. Businesses may also seek additional coverage, such as business interruption insurance, to protect against financial losses due to health crises.

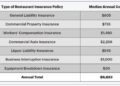

Cost and Affordability of Business General Liability Insurance

When it comes to business general liability insurance, the cost can vary depending on various factors. Understanding how insurers determine these costs and finding ways to manage and potentially reduce them can be crucial for businesses of all sizes.

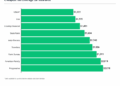

Comparing Cost Across Industries

General liability insurance costs can differ significantly across industries. For example, a small retail store may pay less for coverage compared to a construction company due to the difference in risk exposure.

- Construction Industry: Due to the higher risk of accidents and property damage, businesses in the construction industry may face higher premiums for general liability insurance.

- Technology Start-ups: Start-ups in the tech industry may benefit from lower premiums if they operate in a low-risk environment and have a strong risk management strategy in place.

Tips for Managing Insurance Costs

Businesses can take certain steps to manage and potentially reduce the cost of their general liability insurance:

- Implementing Risk Management Practices: Proactively identifying and addressing potential risks within the business can help lower insurance costs.

- Reviewing Coverage Limits: Adjusting coverage limits based on the specific needs of the business can prevent overpaying for unnecessary coverage.

- Shopping Around: Comparing quotes from multiple insurers can help businesses find the most cost-effective insurance options.

Factors Considered by Insurers

Insurers take various factors into account when determining the cost of a general liability insurance policy:

| Factor | Impact |

|---|---|

| Business Type | Different industries pose different levels of risk, influencing the premium. |

| Claims History | A history of past claims may lead to higher premiums. |

| Location | The geographic location of the business can affect insurance costs due to varying legal environments. |

Final Review

Insurance | Insureon")

As we wrap up our discussion on A Breakdown of Business General Liability Insurance in 2025, it becomes evident that staying informed and proactive is key in navigating the complex realm of insurance. With emerging trends and risks on the horizon, businesses must adapt and prepare for the challenges ahead to ensure adequate protection and coverage.

Popular Questions

What factors influence the cost of general liability insurance?

Insurers consider various factors like industry risk, business size, coverage limits, and claims history when determining the cost of general liability insurance.

How can businesses reduce the cost of their general liability insurance?

Businesses can potentially reduce costs by implementing risk management strategies, maintaining a safe work environment, and reviewing coverage limits regularly to ensure they align with business needs.

{kind=link}